“THE ECONOMY’S BAD, BUT I’M OK”, DATA SHOWS

October 2024 Economic Sentiment Survey Mirrors National Survey Results

It’s that time of year again, when our fund stakes out the local McMinnville Scottish Festival to poll for how people are feeling about their investments. As with last year, the Woodworth Contrarian Fund was the title sponsor of the event, giving us a prominent polling position opposite the main stage (and conveniently close to the VIP booth concessions).

In between conversations with interested attendees, we conducted a poll of 58 willing participants as to their current feelings on the economy, as well as their own personal investments. In exchange, participants received a free Woodworth-branded shot glass. From this poll, a familiar trend emerged:

For those unfamiliar with recent economic sentiment surveys, this bell curve of responses mirrors in miniature more national polls that consistently rank perceptions of the national economy much worse than individuals’ opinions of their own personal investments. This, at first glance, would appear to be contradictory. How can individuals have such divergent opinions of two subjects that are essentially the same in aggregate?

Well, we also asked for a breakdown of where survey participants invested their money, which allows us to make some inferences as to the divergence, if not anything definitive.

Among respondents who were pessimistic about the economy, their investments tended to be more concentrated in cash, which by itself could explain much of the variability. Uninvested cash will tend to lose value over time even when the economy is good, assuming there is no deflation in the value of the money supply. Aside from actively burning your money in a bonfire there’s a good argument to be made that keeping large sums of uninvested cash on hand is one of the worst investments that an individual can make. It is also possible that respondents who were pessimistic about the economy tended to either be worse off financially or simply less sophisticated. For instance, our survey only asked what respondents were currently invested in, and not how much they had invested in total. For an individual without much in assets, it would make sense for a large proportion of their liquid assets to remain in liquid cash to be easily withdrawn and used on short notice. There isn’t much point in investing, after all, if you expect you might need to dip into those assets at some point within the next six months.

Interestingly, pessimistic respondents also tended to have a greater likelihood of having their assets reinvested into their own businesses. Optimists, by contrast, tended to have higher concentrations of investments into risky alternative assets and cryptocurrency. Whether or not this reflects the speculative nature of those sorts of investments attracting optimists, or the other way around (speculative investments engendering optimism in the investors) is difficult to say.

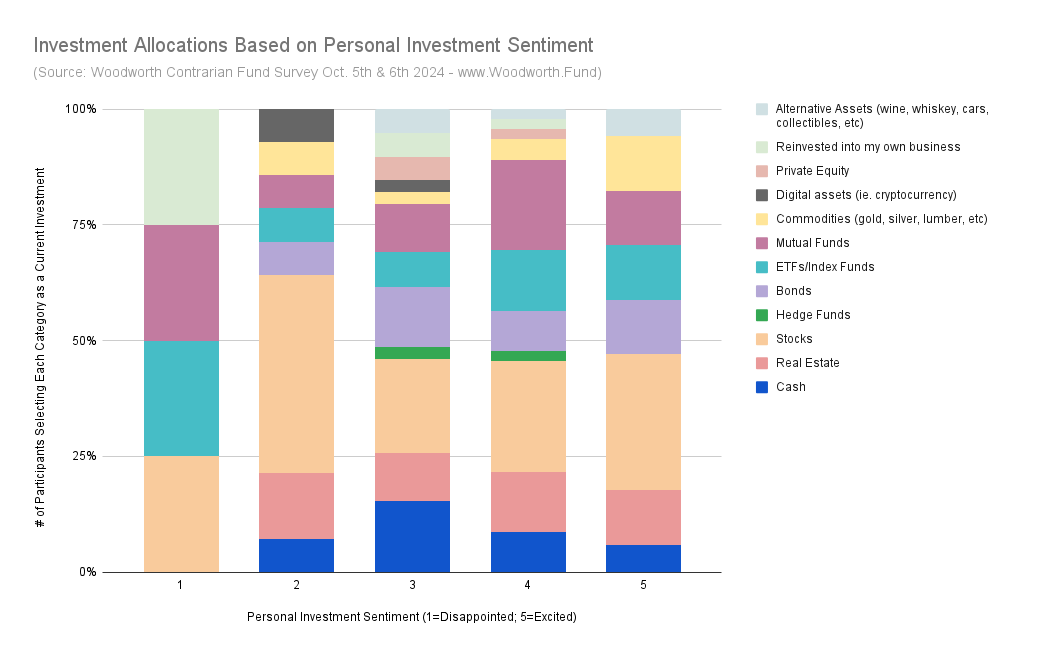

Now, we can also take a look to see how the spread of investments compares when looking at respondents’ self-reported confidence in their personal investments.

Most notably, the trend of pessimists being concentrated in cash mostly disappears, and those respondents invested in crypto reverse from being economically optimistic to being personally pessimistic. Also of note, the survey had very few respondents who rated their own investments at a 1 (“disappointed”) on a scale of one to five, so there is a much murkier picture of what those few pessimistic investors may or may not be allocating their investments toward.

Here, the picture is broadly much more blended. It appears that individuals are simply more confident in their own personal investment decisions regardless of exactly what those personal decisions are, with some exceptions. As stated prior this trend largely mirrors national polls where Americans are more optimistic the closer they are personally to the subject being asked about. For instance, Americans tend to be slightly more optimistic about their local economy than the national economy when asked. This could in part be due to the fact that we are in an election year, but again it is difficult to make any sort of definitive statement as to what is causing the divergence in personal versus national economic sentiment among McMinnville Scottish Festival goers.

Something missing from their portfolio may be a diversification into the Woodworth Contrarian Fund for accredited investors. Now is a great time to diversify your portfolio with an investment into a multi-award-winning fund. An exposure to a value-based contrarian strategy is a unique opportunity for your long term capital that you’re seeking aggressive returns for. With eight years of the Woodworth Fund under management, the Millegan Brothers are trained stock-pickers and experienced venture capital investors with a proven track record. Give us a call today to discuss a liquid investment with independent administration and independently audited monthly statements and a personal relationship.

DEEP ROOTS. STUBBORN GROWTH. OREGON-BASED.

Now is a great time to diversify your portfolio with an investment into an award-winning fund. Call us or visit our website to inquire on an investment today in the Woodworth Contrarian Fund as an accredited investor.

(800) 651-1996 - info@woodworth.fund - www.Woodworth.Fund

Best Contrarian Hedge Fund Managers '22 & ‘23

Contrarian Value-Based Hedge Fund of the Year for 2022-2024

Drew Millegan (left) & Quinn Millegan (right) in front of the Charging Bull in New York City.

About the Managers: Drew Millegan with his brother, Quinn Millegan, (29 and 26 years old respectively) manage the Woodworth Contrarian Stock & Bond Fund, a hedge fund based in McMinnville, Oregon. They grew up in the finance world, and specialize in contrarian investment strategies in the US Public and Private markets.